Table of Contents

- The Bill That Broke the Bank

- The Family’s Shock: A Routine Purchase Gone Wrong

- The Customer Service Struggle: A Marathon of Calls

- Another Layer of Frustration

- Family Vacation Canceled: The Ripple Effect

- The Search for Accountability: Whose Fault Was It?

- Human Error or System Malfunction?

- Official Documentation of the Incident

- The Corporate Struggle to Resolve the Issue

- The Importance of Vigilance in Modern Transactions

The Bill That Broke the Bank

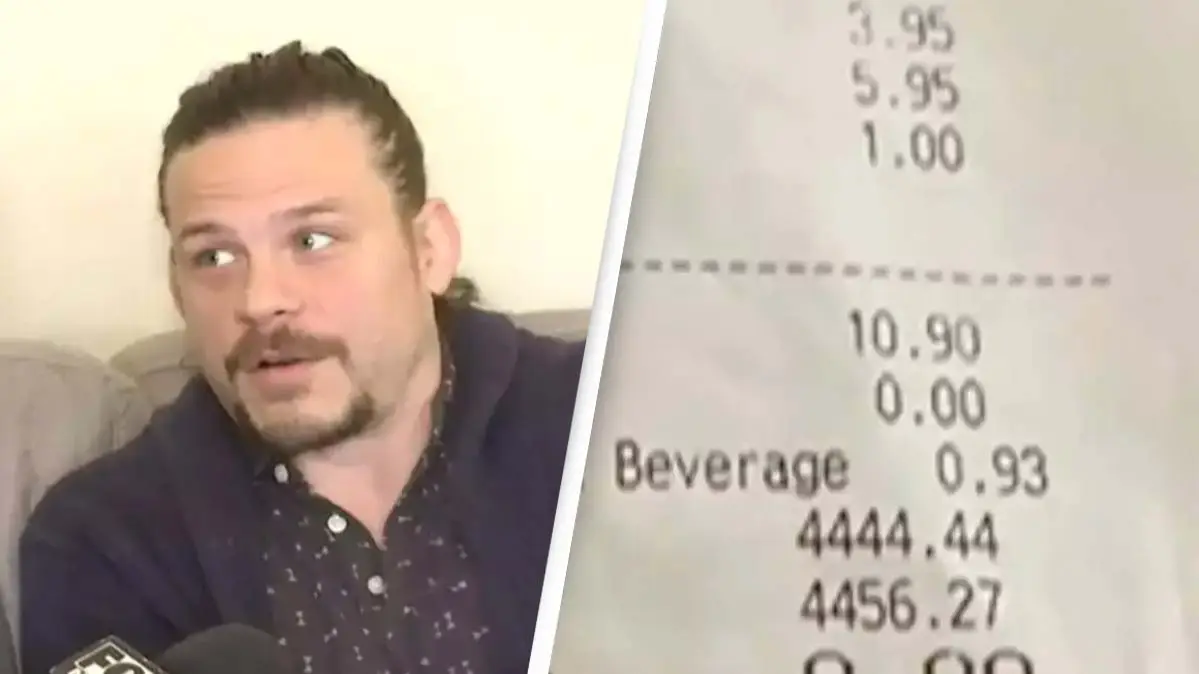

Jesse O’Dell’s order at Starbucks should have been straightforward: a venti caramel frappuccino for himself and an iced Americano for his wife. The total for the two drinks should have hovered around $10. However, the receipt told a different story.

Hidden in the details of the transaction was a line item that defied logic: a $4,444.44 gratuity. The base price of the two beverages was reasonable, but somehow, the system had added an absurd tip, inflating the total to an amount more fitting for an entire month’s rent, not a coffee purchase.

The O’Dells’ checking account, which was intended to cover regular expenses, was drained in an instant. What seemed like a simple setback for most turned into a catastrophic financial blow for a family already juggling the demands of raising four children.

The Family’s Shock: A Routine Purchase Gone Wrong

Deedee O’Dell’s experience at a store counter three days later revealed the magnitude of the error. Expecting to use the same credit card for a routine purchase, she was stunned when the card was declined. A quick check of the account balance showed the horrifying truth: Starbucks had charged them $4,456.27 for two cups of coffee.

The charge was nearly 450 times the cost of their order. Four children watched as their mother tried to process the seemingly impossible situation. This wasn’t just a billing error—it was a financial crisis that would affect the O’Dells for weeks to come.

The Customer Service Struggle: A Marathon of Calls

When the O’Dells realized the extent of the mistake, Jesse immediately contacted Starbucks customer service. What followed was an exhausting process of explaining the issue to representatives who promised swift resolution. Jesse recalled contacting Starbucks’ helpline between 30 and 40 times that day, each call met with assurances that the error would be fixed and a refund would be processed.

Despite the repeated assurances from Starbucks, the O’Dells found themselves in a frustrating loop, waiting for a resolution that seemed elusive. Starbucks promised to mail a refund check, but what followed only added to the mounting frustration.

Another Layer of Frustration

After waiting several days, two checks from Starbucks arrived, intended to reimburse the O’Dells for the excess charge. However, when Jesse tried to deposit the checks, they bounced. The checks had been issued from the Starbucks corporate office but had been returned due to internal processing errors.

Jesse drove to the bank, hoping the issue would finally be resolved. Instead, he found himself with bounced checks, a return trip to the bank, and even more frustration. The O’Dells now faced bank fees in addition to the original error.

Family Vacation Canceled: The Ripple Effect

As the O’Dells’ financial nightmare continued, its effects rippled through their lives. The family had been planning a much-needed vacation, but the unexpected charges and the delays in resolving the issue meant that the vacation had to be canceled. Non-refundable airline tickets became another financial casualty of Starbucks’ mistake.

The O’Dells’ experience was a stark reminder that seemingly minor errors in the digital payment world could have profound and far-reaching consequences. Their family vacation, a rare opportunity to escape the stress of daily life, evaporated along with the money that had been meant for it.

The Search for Accountability: Whose Fault Was It?

As the story gained media attention, Starbucks issued a statement acknowledging the mistake but providing conflicting explanations about its cause. While some company representatives suggested that Jesse himself had made the error, O’Dell was adamant that he had selected the “no tip” option during the transaction.

The dispute raised an important question: was this a result of human error, a software glitch, or something else entirely? Starbucks suggested that the issue was likely a result of a technical malfunction in their system, while some commentators speculated that a manual error had led to the inflated tip.

Human Error or System Malfunction?

As Jesse tried to make sense of the situation, he considered several possibilities. Point-of-sale systems are designed to handle millions of transactions, but their complexity can introduce vulnerabilities. Whether caused by a system malfunction, an incorrect tip entry, or an issue with network connectivity, the end result was the same: the O’Dells were left to deal with the financial fallout.

The lack of clarity about the cause only deepened the O’Dells’ frustration. They couldn’t help but wonder how an everyday purchase had been transformed into a financial crisis.

Official Documentation of the Incident

As the situation grew more dire, Jesse decided to escalate the issue further by filing a report with the Tulsa Police Department. Although criminal fraud seemed unlikely, the police report provided an official record of the event and helped document the financial damage caused by Starbucks’ mistake.

The report added weight to the O’Dells’ claim, giving them an official paper trail to support any potential future legal action. Filing the report marked a turning point in the process, as it indicated the severity of the financial and emotional toll the incident had taken on the family.

The Corporate Struggle to Resolve the Issue

Faced with increasing public scrutiny, Starbucks responded by issuing statements acknowledging the error and attributing it to a mix of technical issues and human error. Despite initial promises of a swift resolution, the process continued to drag on, with no clear resolution in sight.

The company’s response was viewed as inadequate by many, including the O’Dells. While they appreciated the apology, they remained frustrated by the slow pace of the resolution process and the continued inconvenience it caused them.

The Importance of Vigilance in Modern Transactions

The O’Dell family’s experience serves as a cautionary tale for consumers in the digital age. With payment systems increasingly automated, it’s easy for mistakes to go unnoticed until it’s too late. Jesse’s advice is simple: always check receipts immediately and monitor bank statements closely, especially for transactions made through mobile apps or contactless payments.

For businesses, this incident underscores the need for robust error detection and customer service systems to quickly resolve issues and restore customer trust. The O’Dells’ ordeal highlights the importance of clear communication, swift action, and a commitment to addressing mistakes that affect customers’ financial well-being.