Table of Contents

- How Housing Became So Expensive

- The Impact On Middle And Upper Income Families

- Cities Where Housing Costs Are Most Extreme

- Why Supply Has Struggled To Keep Up

- The Growing Gap Between Income And Housing Prices

- The Role Of Investment And Speculation

- Housing Affordability And Economic Inequality

- Government Responses To The Crisis

- The Long Term Outlook For Housing Markets

- A Housing System Under Pressure

- What This Means For The Future

How Housing Became So Expensive

The current housing affordability crisis did not appear overnight. It developed gradually over more than a decade as multiple economic trends converged.

One major factor has been the imbalance between housing supply and demand. Population growth in many metropolitan areas has increased the number of people searching for homes, while construction has struggled to keep up with that demand.

Building new housing units often faces regulatory hurdles, land shortages, and rising construction costs. These challenges have slowed development in many regions, particularly in areas with strong job markets.

At the same time, low interest rates during earlier periods encouraged home buying and investment in real estate. Cheap borrowing made mortgages more accessible and stimulated housing demand.

When demand rises faster than supply, prices inevitably climb.

Over time this imbalance pushed home prices to levels that outpaced income growth, gradually making housing less affordable even for households with strong earnings.

The Impact On Middle And Upper Income Families

Traditionally, housing assistance programs were designed to support households earning well below the national median income. The idea was to provide a safety net for families facing economic hardship.

However, the dramatic rise in home prices has shifted this dynamic in several cities.

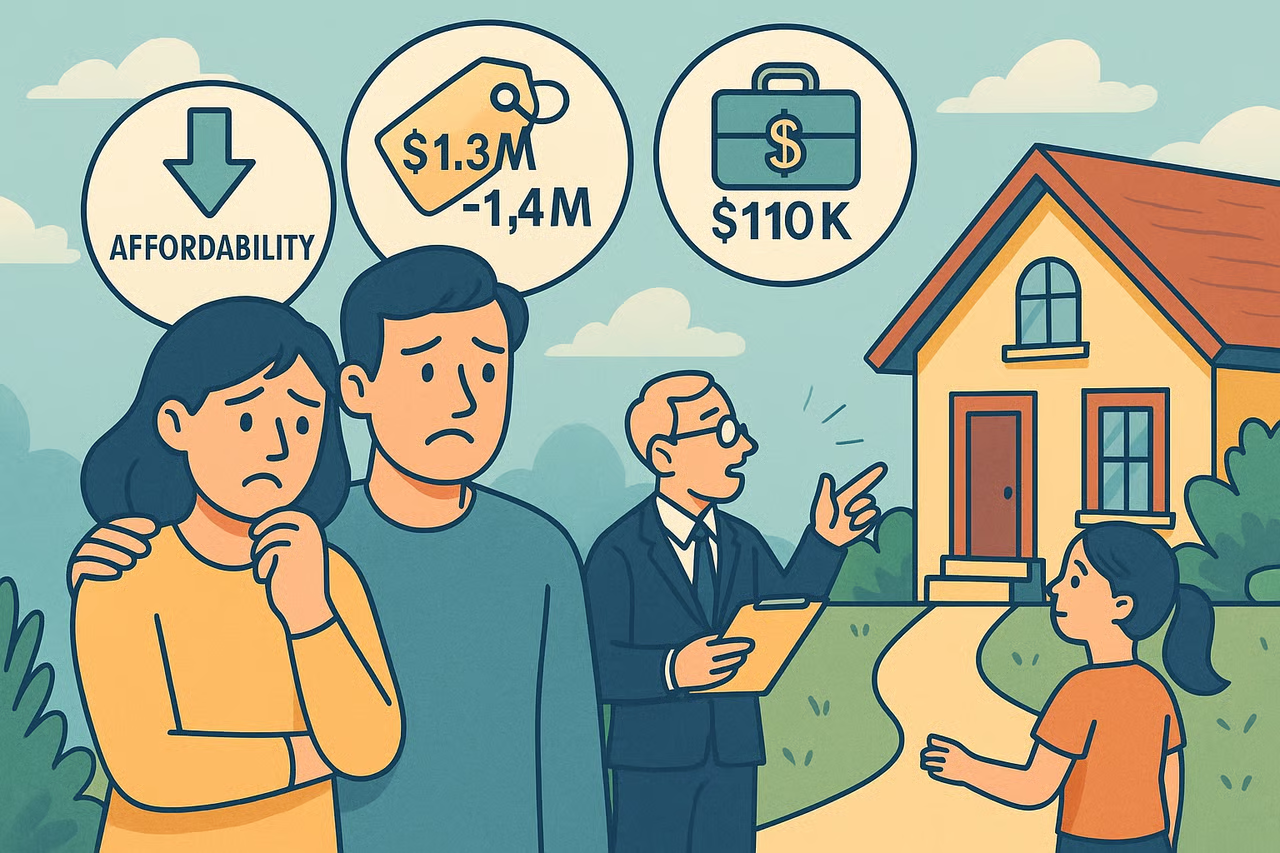

In regions with extremely high housing costs, the income threshold for assistance has increased dramatically. Some programs now include households earning far more than what would historically be considered middle class.

In practical terms, this means a family earning $200000 a year may still struggle to purchase a home in certain metropolitan areas.

Mortgage payments, property taxes, insurance, and maintenance costs can easily exceed what even relatively high salaries can comfortably support.

This shift highlights how housing affordability has become a structural issue affecting a wide range of income levels.

Cities Where Housing Costs Are Most Extreme

The affordability crisis is particularly severe in cities with strong economic growth and limited housing supply. Urban areas that attract large numbers of workers often experience the fastest price increases.

Cities with thriving technology, finance, and entertainment industries have seen housing demand surge in recent years.

As companies expand and high paying jobs become concentrated in certain regions, more people compete for a limited number of homes.

In some metropolitan areas, the median home price has climbed well above one million dollars. Mortgage payments on properties at these price levels can easily exceed several thousand dollars per month.

Even households with substantial incomes can find themselves stretched financially when attempting to buy homes in these markets.

For renters, the situation is often just as challenging. Rental prices have climbed steadily, sometimes rising faster than wages.

Why Supply Has Struggled To Keep Up

Housing shortages are not simply the result of increased demand. Several structural factors have limited how quickly new homes can be built.

Zoning regulations often restrict the types of housing that developers can construct in certain neighborhoods. In some areas, large portions of residential land are reserved exclusively for single family homes.

While such rules can preserve neighborhood character, they also limit the density of housing that can be built.

Construction costs have also risen sharply in recent years. Labor shortages, supply chain disruptions, and rising material prices have increased the cost of building new homes.

Developers facing higher costs often prioritize building more expensive properties that generate higher returns.

This dynamic can reduce the number of affordable housing units entering the market.

The Growing Gap Between Income And Housing Prices

One of the most troubling aspects of the housing crisis is the widening gap between income growth and housing costs.

While wages have increased in some industries, they have not kept pace with the rapid rise in property prices.

Economists often measure affordability by comparing the cost of housing with household income. When housing consumes a large share of income, financial stability becomes more difficult to maintain.

Many experts suggest that housing costs should ideally remain below thirty percent of a household’s income.

In many American cities today, families are spending significantly more than that threshold.

For some households, housing costs consume forty or even fifty percent of monthly income.

This leaves less money available for healthcare, education, transportation, and savings.

The Role Of Investment And Speculation

Another factor influencing housing prices is the increasing role of investors in the real estate market.

Institutional investors, investment funds, and private buyers have purchased large numbers of residential properties in recent years. Some of these properties are rented out, while others are held as long term investments.

While investment can stimulate housing development, it can also intensify competition for available homes.

When investors compete with individual buyers, prices can rise more quickly.

Some analysts argue that speculative investment has contributed to housing shortages in certain markets.

Others note that investors often purchase properties in areas already experiencing strong price growth, reinforcing existing trends.

Regardless of the exact impact, the presence of large scale investment has become an increasingly visible feature of modern housing markets.

Housing Affordability And Economic Inequality

The housing crisis has also deepened concerns about economic inequality. When housing becomes more expensive, lower income households often face the greatest difficulties.

However, the expansion of affordability challenges into higher income brackets suggests that the problem has become systemic.

If even well paid professionals struggle to afford homes in major cities, the implications for younger workers and middle income families become even more serious.

Many young adults now delay purchasing homes or starting families because housing costs are simply too high.

This trend can have long term demographic and economic consequences.

Home ownership has historically been one of the primary ways households build wealth over time.

When fewer people can access the housing market, wealth accumulation patterns may change significantly.

Government Responses To The Crisis

Governments at local, state, and federal levels have begun exploring various strategies to address the housing shortage.

Some policies focus on increasing housing supply by encouraging new construction. Others aim to expand assistance programs or provide incentives for affordable housing development.

Reforms to zoning regulations are also being discussed in many cities.

Allowing higher density housing such as apartment buildings or townhomes can increase the number of available units in desirable areas.

However, these reforms often face political resistance from existing residents concerned about neighborhood changes.

Balancing housing affordability with community preferences remains one of the most challenging aspects of housing policy.

The Long Term Outlook For Housing Markets

Predicting the future of housing prices is difficult because markets depend on multiple factors including interest rates, population growth, and economic conditions.

Higher interest rates can slow housing demand by making mortgages more expensive. This can reduce price growth in some markets.

However, if supply shortages persist, prices may remain elevated even during economic slowdowns.

Some economists believe that addressing the housing crisis will require sustained efforts over many years.

Building enough new homes to match demand is a long term process that involves regulatory reform, investment, and coordinated planning.

A Housing System Under Pressure

The revelation that households earning $200000 may qualify for housing assistance highlights how dramatically the housing landscape has changed.

What was once considered a comfortable income in many regions now struggles to keep pace with the realities of the modern housing market.

The situation underscores a broader shift in economic conditions affecting millions of Americans.

Housing affordability is no longer a challenge limited to a specific income group. It has become a widespread issue that affects communities across the country.

As policymakers, developers, and communities search for solutions, the stakes remain high.

Access to stable and affordable housing influences economic mobility, family stability, and the overall health of society.

What This Means For The Future

The expanding housing affordability crisis suggests that the traditional relationship between income and home ownership is undergoing profound change.

If housing prices continue rising faster than wages, more households may find themselves priced out of the market.

This possibility has prompted increasing calls for policy reforms aimed at boosting supply and stabilizing prices.

The path forward will likely involve a combination of strategies including expanded construction, updated zoning laws, and targeted assistance programs.

Ultimately, the goal is to restore a housing system where earning a strong income once again provides realistic access to stable housing.