Table of Contents

- Mortgage Rates Surge, Crushing Homebuyers’ Plans

- How Global Events Are Impacting the Housing Market

- The Financial Impact on Prospective Homebuyers

- A Weakened Spring Housing Market

- The Changing Landscape of Homeownership in 2026

- Will Higher Mortgage Rates Lead to Market Slowdown?

- The Broader Economic Context of Rising Rates

- How Will Buyers and Sellers Adapt to New Conditions?

- Conclusion: A Housing Market in Transition

Mortgage Rates Surge, Crushing Homebuyers’ Plans

When news broke that mortgage rates were climbing again, the immediate effect on the spring housing market was one of dread for aspiring homeowners. For those eagerly awaiting the warmer months to make their move, 2026’s housing outlook seemed promising. With new construction picking up and the market recovering from previous economic downturns, experts predicted a strong season ahead. But as borrowing costs spiked unexpectedly, those plans have now been shattered. A sharp increase in mortgage rates is making it more difficult for homebuyers to secure affordable loans, and the global economic factors at play are not helping matters.

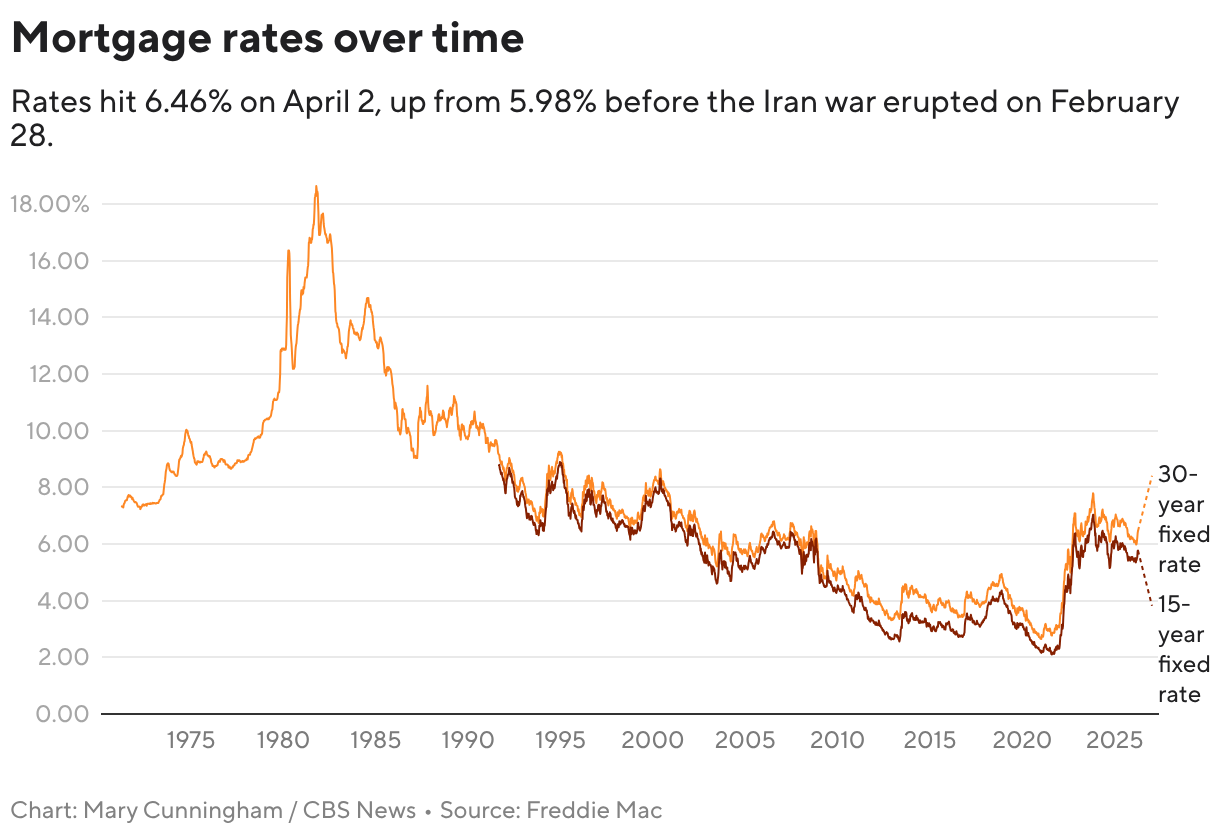

The rate on a conventional 30-year home loan has surged to 6.46% as of early April 2026, marking the highest point since September 2025. Mortgage rates, which had dipped below 6% just weeks ago, have now sharply reversed course, much to the dismay of first-time buyers and those looking to upgrade. This sudden increase in borrowing costs is tied not only to domestic inflation but also to global economic concerns, particularly the ongoing war in the Middle East. Economists have pointed to inflationary pressure linked to the war’s effect on global markets, particularly government bond yields. Mortgage rates are heavily influenced by the yield on the 10-year Treasury bond, and with those yields rising, rates on home loans follow suit.

How Global Events Are Impacting the Housing Market

The connection between rising mortgage rates and the war in Iran may not seem immediately obvious to many, but it has become a crucial factor in the economic landscape. The uncertainty surrounding the war and the accompanying rise in government bond yields has led to fears of prolonged inflation. As Mike Fratantoni, chief economist at the Mortgage Bankers Association, explained, when inflation climbs, investors demand higher returns on bonds, including mortgage-backed securities, to compensate for the higher inflation. This dynamic naturally pushes mortgage rates higher.

Before the war, many were hopeful that the housing market would get a boost this year. With a slight uptick in inventory and construction, coupled with lower year-over-year listing prices, it seemed like a perfect storm for a thriving spring buying season. Yet, the sudden rise in mortgage rates has complicated this picture. The higher cost of borrowing is making homes less affordable for many, which is contributing to a slowdown in market activity as buyers and sellers alike reassess their strategies.

The Financial Impact on Prospective Homebuyers

For potential homebuyers like Devan Post, a corporate controller from Minnesota, the surge in mortgage rates is more than just a minor inconvenience. She had initially received a favorable rate quote of 5.85% for a 30-year fixed-rate mortgage but watched in disbelief as rates climbed to 6.49% after the war in the Middle East. While she and her husband were still able to make an offer on a home, the extra $265 per month they would need to pay as a result of the rate hike is a bitter pill to swallow. Over the life of their 30-year loan, this translates into an additional $95,400, a sum that could have been better spent elsewhere.

These sudden increases in mortgage rates create a significant burden for families trying to navigate an already difficult housing market. For many, the financial adjustments needed to make the numbers work can cause them to reconsider their plans entirely. It’s a frustrating reality for anyone hoping to buy a home, especially after having believed they were finally in a position to secure an affordable loan.

A Weakened Spring Housing Market

With the housing market traditionally heating up during the spring months, many experts were initially optimistic about 2026. The slight increase in inventory, combined with a drop in year-over-year listing prices, seemed to be a recipe for success. However, with mortgage rates rising sharply, this optimism has waned.

The Mortgage Bankers Association (MBA) recently downgraded its forecast for home sales in 2026, adjusting its projection from an 8% increase to a more modest 5% rise. This is a clear indication that the surge in mortgage rates is dampening enthusiasm in the market, as higher borrowing costs limit the number of buyers able to afford new homes. Some economists are predicting that rising rates may send many potential buyers and sellers to the sidelines, further slowing an already tepid market.

While it’s too early to tell whether the spring homebuying season will be entirely derailed, the early signs are not promising. The MBA’s purchase index, which tracks mortgage applications, fell 3% on April 1 compared to the previous week, signaling a dip in demand.

The Changing Landscape of Homeownership in 2026

For many, the dream of homeownership in 2026 has become harder to attain. Higher mortgage rates are making it more difficult for prospective buyers to find homes within their budget. As rates climb above 6%, many first-time buyers who had previously hoped to secure an affordable loan now find themselves priced out of the market.

Moreover, as rates continue to rise, the affordability gap widens for both first-time buyers and those looking to upgrade to a larger home. For individuals like Devan Post, the possibility of securing a home in their desired price range feels less likely as each week passes, with rates inching higher and home prices remaining elevated. Buyers who had initially been eager to move forward are now second-guessing their decisions, unsure if the timing is right.

The persistent rise in mortgage rates also poses challenges for homeowners looking to refinance their current loans. With refinancing becoming more expensive, many homeowners are being forced to hold onto their current mortgages longer than anticipated, limiting their ability to tap into home equity or adjust their loans to better reflect changing financial conditions.

Will Higher Mortgage Rates Lead to Market Slowdown?

As mortgage rates continue to climb, experts are wondering if the housing market will experience a full-fledged slowdown in 2026. While some economists predict that the market may cool due to higher mortgage costs, others believe that buyers may still rush to secure a home before rates increase even further. The idea is that with rates above 6%, buyers might feel the urgency to lock in a rate before they rise higher, creating a potential window of opportunity for sellers.

However, the overall trend points toward a softer market as higher mortgage rates take their toll. The Federal Reserve’s decision to keep interest rates higher for longer, in an effort to curb inflation, means that mortgage rates are unlikely to dip back down anytime soon. This will likely keep pressure on the housing market for the remainder of the year.

The Broader Economic Context of Rising Rates

Mortgage rates are not only influenced by global events but also by the broader economic context. With inflation still above the Federal Reserve’s target of 2%, many economists are predicting that the central bank will refrain from cutting its benchmark rate for all of 2026. This policy shift, coupled with rising inflation and the global tensions created by the Iran war, suggests that mortgage rates will likely stay elevated for the foreseeable future.

As Mike Fratantoni noted, investors in mortgage-backed securities demand higher returns to account for the risks posed by inflation. This increased demand for higher yields on bonds directly contributes to the higher rates seen in the mortgage market. For homebuyers, this means that the dream of homeownership may become more distant unless they can secure a loan before rates rise further.

How Will Buyers and Sellers Adapt to New Conditions?

With mortgage rates continuing to climb, both buyers and sellers will need to adapt to the changing landscape. Buyers may have to rethink their budgets and adjust their expectations, while sellers may need to reassess their pricing strategies to account for the decline in demand. It’s likely that some buyers will be forced to scale back their plans and consider more affordable options or delay their home search altogether until the market stabilizes.

Sellers may need to get creative with pricing strategies, offering incentives or making improvements to attract potential buyers. In the end, it’s clear that both sides of the market will have to adjust to a new reality where borrowing costs are higher and demand is more tempered.

Conclusion: A Housing Market in Transition

The surge in mortgage rates has thrown a wrench into the housing market, disrupting what many hoped would be a strong 2026 spring season. While higher rates are a natural byproduct of inflation and global economic uncertainty, their impact on prospective homeowners has been swift and significant. For buyers like Devan Post, the dream of homeownership has become more complicated, with increased costs and limited options.

As mortgage rates remain elevated, it is clear that the housing market in 2026 will be far from what many had envisioned. Whether this will result in a full market slowdown or simply a shift in buyer behavior remains to be seen. However, one thing is certain: higher mortgage rates are here to stay, at least for the near future, and the long-awaited rebound in the housing market may have to wait.